Meta Description: Master your money with our 2026 personal budget plan guide. Learn the 50/30/20 rule, AI-powered tracking, and how to inflation-proof your financial future today.

Building a personal budget plan in 2026 is no longer just about tracking receipts or balancing a checkbook. In an era of digital wallets, “subscription creep,” and rapid cost-of-living adjustments, your budget must be as dynamic as your lifestyle.

Whether you are trying to pay off student debt using the Debt Avalanche method or looking to integrate your cryptocurrency assets into your daily spending view, a structured plan provides the mental clarity needed to reach financial wellness. This guide will walk you through the “what, why, and how” of modern budgeting, from the classic 50/30/20 rule to high-tech AI-predictive forecasting.

Why You Need a Budget Plan Now

TL;DR: A budget isn’t a restriction; it’s a GPS for your goals. It prevents “vibe-spending” and ensures your money supports your actual priorities.

A personal budget plan is a roadmap for your money. Without it, you are susceptible to “vibe-spending”—the tendency to spend based on social media trends or emotional impulses rather than financial capacity. With the Consumer Price Index (CPI) and inflation fluctuations remaining a concern in 2026, a budget acts as a buffer.

It allows you to identify “disposable income optimization” opportunities—finding money you didn’t know you had by cutting “ghost subscriptions” and optimizing your fixed costs.

Preparing Your Data for 2026

Before you can build a house, you need the right materials. In budgeting, that means raw data.

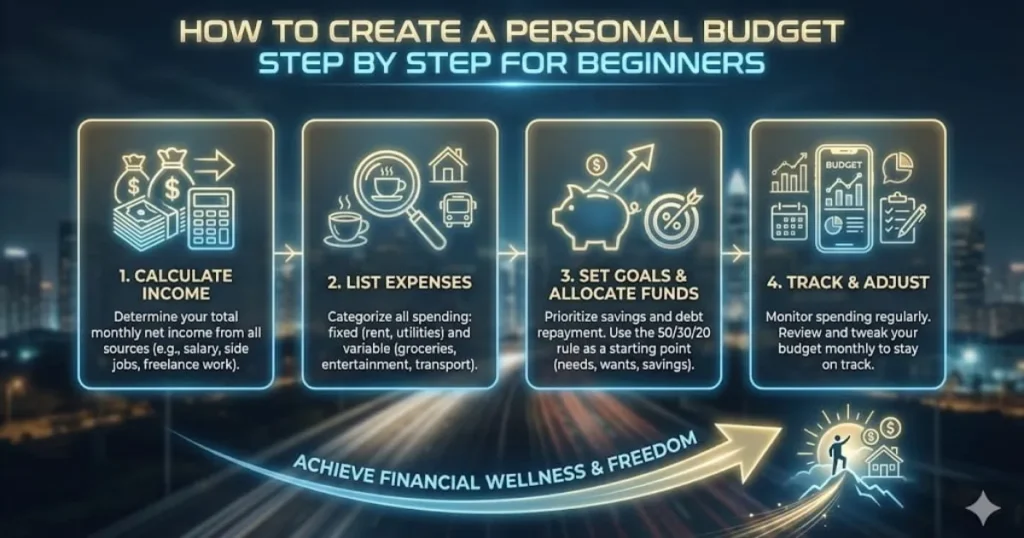

1. Calculate Your True Net Income

Many beginners make the mistake of budgeting based on their gross salary. Always use your Net Income (take-home pay).

- B2C Tip: Include your base salary, but also account for side hustles or freelance gigs.

- The 2026 Edge: If your income is irregular, calculate a 6-month average to create a “baseline budget.”

2. Audit Your Subscriptions (The AI Way)

“Subscription creep” is the silent killer of modern budgets. In 2026, the average household pays for over 12 recurring services.

- Action Step: Use an AI-predictive budgeting tool to scan your bank statements. These tools can identify price hikes in your Netflix, cloud storage, or gym memberships that you might have missed.

3. Sync Your Digital Wallets

Financial wellness in 2026 requires a “birds-eye view.” Ensure your plan accounts for:

- Traditional bank accounts.

- Digital payment apps (Venmo, PayPal).

- Cryptocurrency Wallets: Use Open Banking APIs to safely link your Coinbase or MetaMask accounts so your net worth reflects your total liquidity.

Choosing Your Budgeting Methodology

There is no “perfect” system, only the system that you will actually stick to.

The 50/30/20 Rule (Best for Beginners)

This is the gold standard for simplicity. You divide your after-tax income into three buckets:

- 50% Needs: Rent/Mortgage, utilities, groceries, and minimum debt payments.

- 30% Wants: Dining out, travel, and non-essential shopping.

- 20% Savings & Debt Repayment: Emergency fund, 401(k) contributions, and extra debt payments.

Zero-Based Budgeting (Best for Detail-Oriented)

With this method, every single dollar is assigned a “job” until your income minus expenses equals exactly zero. This prevents money from “disappearing” into mindless spending.

The “Pay Yourself First” Method (Best for Minimalists)

Instead of budgeting what is left over, you automate your savings and debt payments the moment your paycheck hits. You are then free to spend the remainder without guilt.

Step-by-Step: How to Build Your 2026 Budget Plan

Step 1: List Fixed vs. Variable Expenses

Fixed expenses stay the same (rent, car insurance). Variable expenses change (groceries, electricity). In 2026, treat your “Digital Subs” as a separate category to monitor them more closely.

Step 2: Establish an “Inflation Buffer”

In the current economic climate, prices can shift mid-month.

- Pro Tip: Set aside a 3%–5% “Inflation Buffer” in your monthly expenses. If you don’t use it by the end of the month, move it directly into your Emergency Fund.

Step 3: Set SMART Financial Goals

Your budget should have a “Why.”

- Specific: “Save $5,000 for a down payment.”

- Measurable: “Track progress via my banking app.”

- Achievable: “Based on my 20% savings rate.”

- Relevant: “To stop renting by 2027.”

- Time-bound: “Within 12 months.”

Step 4: Choose Your Tools

| Tool Type | Examples | Best For |

| AI-Powered Apps | YNAB, Monarch Money | Automation & Predictive alerts |

| Manual Spreadsheets | Excel, Google Sheets | Privacy & Total control |

| Physical Systems | Cash Envelopes | Curbing overspending |

Managing Debt: Snowball vs. Avalanche

If your budget is currently “red” (spending more than you earn), you need a debt strategy.

- Debt Snowball: Pay the smallest balance first for psychological “wins.”

- Debt Avalanche: Pay the highest-interest debt first to save the most money over time.

Integrating these into your personal budget plan is essential for long-term financial planning.

Common Budgeting Mistakes to Avoid

- Forgetting Irregular Expenses: Amazon Prime renewals, car registrations, and holiday gifts should be handled via “Sinking Funds” (saving small amounts monthly for a future large expense).

- Being Too Strict: If you cut out all “wants,” you will eventually “binge-spend.” Build in a small amount of “Fun Money.”

- Ignoring Data Security: When using budgeting apps, ensure they use bank-level encryption and are YMYL (Your Money Your Life) compliant. Never share your private keys for crypto wallets with a third-party app.

People Also Ask (FAQs)

How do I account for inflation in my 2026 budget?

The best way is to build a 3-5% “Buffer Category” into your monthly plan. Additionally, review your grocery and utility categories quarterly, as these are most sensitive to Consumer Price Index (CPI) changes.

What is a realistic emergency fund amount for 2026?

Most experts recommend 3–6 months of Fixed Expenses. However, if you are a freelancer with irregular income, aiming for 9 months provides a more secure safety net.

How do I sync my crypto wallet with my budget plan?

Most modern FinTech apps use secure Open Banking APIs (like Plaid) to view your balances. You should only grant “read-only” access to your digital assets to maintain security.

Is the 50/30/20 rule still relevant with high rent?

In “High Cost of Living” (HCOL) areas, your “Needs” might consume 60% or 70% of your income. In this case, adjust to a 70/20/10 split, prioritizing your 10% savings until your income increases.

What is “predictive cash flow” in budgeting?

Predictive cash flow uses AI to look at your historical spending patterns and warn you before you overspend. For example, it might alert you that your upcoming electric bill will be higher due to a heatwave.

How can I stop “subscription creep”?

Perform a “Digital Audit” every 90 days. If you haven’t used a service in the last 30 days, cancel it. Many 2026 budgeting apps now offer a one-click “Cancel Service” feature.

Can I budget with a partner?

Yes. Many couples use a “Joint-Expense” budget while maintaining separate “Personal Want” accounts. This balances shared responsibility with individual autonomy.

Conclusion

Making a personal budget plan is the single most effective way to reduce financial anxiety. By combining time-tested methods like the 50/30/20 rule with 2026 technology like AI-predictive tracking, you can transform your relationship with money.

Read More: Personal Budgeting Tips………….